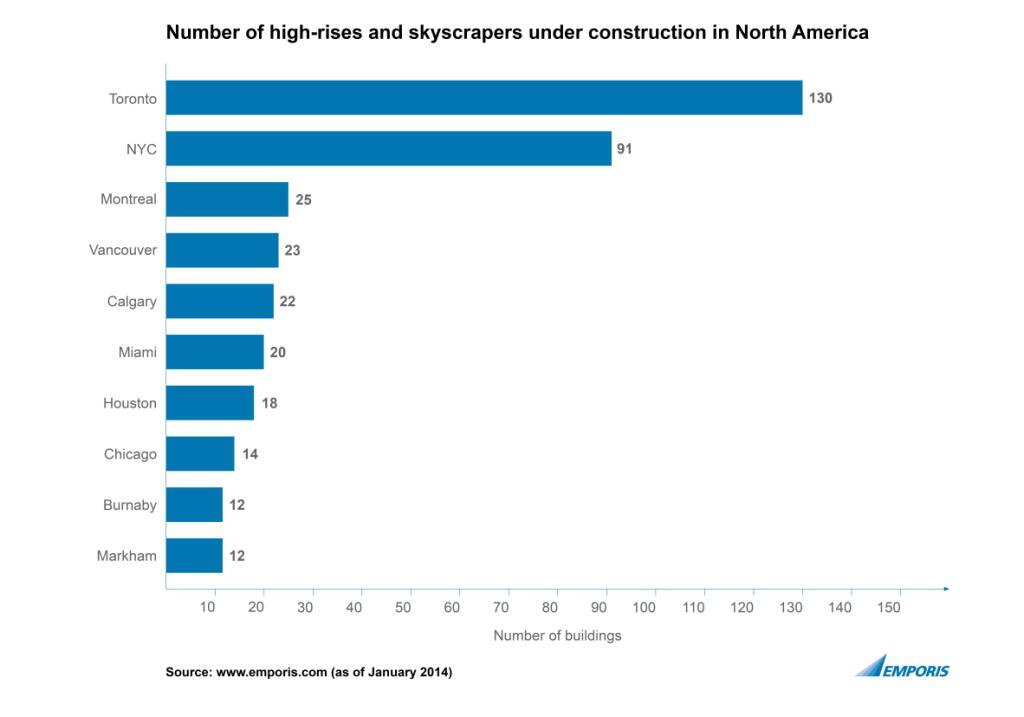

Wednesday, 22 January 2014

Vancouver ranks 4th in North America for high rise construction.

Wednesday, 15 January 2014

Australia posted terrible job numbers, AUDUSD plummets.

"The Australian Bureau of Statistics has just released the December employment report, which was a terrible number no matter which way you cut it.

Employment in Australia fell by 22,600. But the huge fall in full-time unemployment of 31,600 is the big shock for markets, and puts a big question mark on the recovery at the moment.

But it is the contracting participation rate (think people in the workforce or actively looking for jobs) which is really holding the unemployment rate below 6%."

AUDUSD down 3% in 3 days. Sounds familiar?

Thursday, 9 January 2014

加币如预测继续贬值 / CAD Continues its descent, as expected

GF 早在2012年就看空澳币及加币

在加币兑美金过par 时 (2012下半年),GF 已把过半 当时手上的加币换为美金。

总投资portfolio 在2013年初 约60%为美金/美股

www.westca.com/Forums/...ml#5045013

forum.iask.ca/showpost...stcount=21

澳币从2012年春已对美金下跌了 18%。

加币从2012年底对美金已跌了 11%

GF 继续看跌加币,且将在未来加币短期回涨的时机购入更多美金。

若这里有同样中期看跌加币的朋友,而手上还有大温投资房的话,应仔细想想如何应对这个加币贬值的(可能)中长期趋势。

Brief Translation:

As early as early 2012 I had been bearish on AUD and CAD.

Back when CADUSD>1.00, I had already converted over 50% of my cash/investment holdings into USD. As of early 2013, 60% of my entire investment portfolio was in USD.

Since Spring 2012, AUDUSD had already declined 18% vs USD

Since Late 2012, CADUSD had already declined 11% vs USD

I continue to be mid-term bearish on CAD and plan to purchase more USD when opportunities arise down the road.

If you are an owner of investment properties in Vancouver, and are also at least mid-term bearish on CAD, you should know what to do next.

在加币兑美金过par 时 (2012下半年),GF 已把过半 当时手上的加币换为美金。

总投资portfolio 在2013年初 约60%为美金/美股

www.westca.com/Forums/...ml#5045013

forum.iask.ca/showpost...stcount=21

澳币从2012年春已对美金下跌了 18%。

加币从2012年底对美金已跌了 11%

GF 继续看跌加币,且将在未来加币短期回涨的时机购入更多美金。

若这里有同样中期看跌加币的朋友,而手上还有大温投资房的话,应仔细想想如何应对这个加币贬值的(可能)中长期趋势。

Brief Translation:

As early as early 2012 I had been bearish on AUD and CAD.

Back when CADUSD>1.00, I had already converted over 50% of my cash/investment holdings into USD. As of early 2013, 60% of my entire investment portfolio was in USD.

Since Spring 2012, AUDUSD had already declined 18% vs USD

Since Late 2012, CADUSD had already declined 11% vs USD

I continue to be mid-term bearish on CAD and plan to purchase more USD when opportunities arise down the road.

If you are an owner of investment properties in Vancouver, and are also at least mid-term bearish on CAD, you should know what to do next.

Sunday, 5 January 2014

Sample Calculation: Projected Net Worth 2013-2016 - Renting vs Buying

For those of us renting by choice, we need to regularly reassess whether this "choice" is still financially sound.

I had just drafted a rough spreadsheet comparing renting vs buying, in relative approximation of my personal situation.

The values in this spreadsheet assumed the following:

1. "Annual Savings Pre-housing" = After-tax income minus all expenditures other than housing-related expenditures

* due to privacy reasons, the income & current savings amount have been altered somewhat

2. Current rental accommodation = 4BR SFH worth ~800k market value. Rent had stayed the same for 2 years & expected to stay fixed for foreseeable future due to myself being a "desirable tenant".

3. Target property is newer SFH in Van East / Burnaby & Surrounding neighborhoods, current market value ~$1.3-$1.5M.

4. Despite my prediction that Vancouver RE in my target price range will decline in value in the coming years, let us just assume here that $1.4M-range Van E / Burnaby SFH price will stay unchanged between 2013 and end of 2015.

5. For simplicity, assume annual income & non-housing expenditure stay the same.

6. If I buy in 2016, I will place a larger down payment (500k) than in 2013 (350k), due to the money saved by renting.

7. Assume the renter's Return on Investment of his savings = 3%/year (let's be conservative)

8. Assume the home-owner's repair/maintenance cost at only $2000/year (in reality often higher, unless brand new homes)

A. We can see that if I stay renting from 2013-2015 inclusive, and if the $1.4M target property price stays unchanged, my networth by the end of 2015 will be over $100k higher renting (551k) vs buying (448k).

B. In Scenario 1, where I purchase the property at same price as 2013, but mortgage rate increased from 2.89% to 3.09% (fixed rates may already be higher, but variable rates can very possibly stay low even by 2016), by end of 2016 my networth will be $62k higher by delaying home purchase to 2016, than buying in 2013.

C. In Scenario 2, where Target Property price falls 10% by early 2016 vs 2013. By end of 2016, my networth will be $543.8k if I buy in 2016, vs $337.6k if I bought in 2013. A difference of $206k.

D. In Scenario 3, where Target Property price actually gains 5% by early 2016. By end of 2016, my networth will be $537k if I buy in 2016, vs 548k if I bought in 2013. In this case buying in 2013 wins vs delaying purchase.

E. In Scenario 4, where Target Property price remained unchanged, but mortgage rate increased to 3.39% (let's say that's variable rate mortgage), in terms of networth, delaying purchase still beats buying early.

To conclude, as long as Target Property appreciates <5% between 2013 and end of 2015, then buying in 2016 beats buying in 2013, in terms of personal networth, in this particular case. If price stays the same, then the renter beats the 2013-buyer by over $100k in networth. If price declines 10%, then the renter beats the 2013-buyer by over $200k in networth by end of 2015.

I had just drafted a rough spreadsheet comparing renting vs buying, in relative approximation of my personal situation.

The values in this spreadsheet assumed the following:

1. "Annual Savings Pre-housing" = After-tax income minus all expenditures other than housing-related expenditures

* due to privacy reasons, the income & current savings amount have been altered somewhat

2. Current rental accommodation = 4BR SFH worth ~800k market value. Rent had stayed the same for 2 years & expected to stay fixed for foreseeable future due to myself being a "desirable tenant".

3. Target property is newer SFH in Van East / Burnaby & Surrounding neighborhoods, current market value ~$1.3-$1.5M.

4. Despite my prediction that Vancouver RE in my target price range will decline in value in the coming years, let us just assume here that $1.4M-range Van E / Burnaby SFH price will stay unchanged between 2013 and end of 2015.

5. For simplicity, assume annual income & non-housing expenditure stay the same.

6. If I buy in 2016, I will place a larger down payment (500k) than in 2013 (350k), due to the money saved by renting.

7. Assume the renter's Return on Investment of his savings = 3%/year (let's be conservative)

8. Assume the home-owner's repair/maintenance cost at only $2000/year (in reality often higher, unless brand new homes)

A. We can see that if I stay renting from 2013-2015 inclusive, and if the $1.4M target property price stays unchanged, my networth by the end of 2015 will be over $100k higher renting (551k) vs buying (448k).

B. In Scenario 1, where I purchase the property at same price as 2013, but mortgage rate increased from 2.89% to 3.09% (fixed rates may already be higher, but variable rates can very possibly stay low even by 2016), by end of 2016 my networth will be $62k higher by delaying home purchase to 2016, than buying in 2013.

C. In Scenario 2, where Target Property price falls 10% by early 2016 vs 2013. By end of 2016, my networth will be $543.8k if I buy in 2016, vs $337.6k if I bought in 2013. A difference of $206k.

D. In Scenario 3, where Target Property price actually gains 5% by early 2016. By end of 2016, my networth will be $537k if I buy in 2016, vs 548k if I bought in 2013. In this case buying in 2013 wins vs delaying purchase.

E. In Scenario 4, where Target Property price remained unchanged, but mortgage rate increased to 3.39% (let's say that's variable rate mortgage), in terms of networth, delaying purchase still beats buying early.

To conclude, as long as Target Property appreciates <5% between 2013 and end of 2015, then buying in 2016 beats buying in 2013, in terms of personal networth, in this particular case. If price stays the same, then the renter beats the 2013-buyer by over $100k in networth. If price declines 10%, then the renter beats the 2013-buyer by over $200k in networth by end of 2015.

Thursday, 2 January 2014

BC Assessment Roll is out (w/ my short spreadsheet tracking 2012-2014 assessments of a few properties)

http://www.vancouversun.com/business/real-estate/Vancouver+west+side+east+side+divide+narrows/9343430/story.html

I did keep a small spreadsheet tracking the assessment prices of certain buildings since 2012. Most of those buildings are either close to ones I've lived in before, or are close to addresses of my relatives/friends.

A. Let’s start with my current rental house (put up for rent in 2012, where landlord/builder tried to sell for $860,000 but no takers):

Assessment:

2012: 815000

2013: 809000

2014: 793000

B. Condo in E Van: (2012, 2013, 2014)

2101-3663 CROWLEY DR 472000 436000 423000

(bought 455000 2/20/2011)

502-3663 CROWLEY DR 336000 309000 299000

(bought 318000 1/28/2011)

2101-3663 CROWLEY DR 472000 436000 423000

(bought 455000 2/20/2011)

502-3663 CROWLEY DR 336000 309000 299000

(bought 318000 1/28/2011)

C. Condo in Burnaby: (2012, 2013, 2014)

607-7088 18TH AVE 394000 391000 387000

(bought 406000 5/2/2011)

1902-7088 18TH AVE 483000 479000 473000

(bought 462000 5/15/2011)

701-6688 ARCOLA ST 443000 446000 441000

(bought 470000 5/31/2011)

1105-6688 ARCOLA ST 411000 406000 402000

(bought 460000 7/12/2011)

607-7088 18TH AVE 394000 391000 387000

(bought 406000 5/2/2011)

1902-7088 18TH AVE 483000 479000 473000

(bought 462000 5/15/2011)

701-6688 ARCOLA ST 443000 446000 441000

(bought 470000 5/31/2011)

1105-6688 ARCOLA ST 411000 406000 402000

(bought 460000 7/12/2011)

D. Townhouse in Richmond: (2012, 2013, 2014)

8-5580 MONCTON ST 711000 703000 688000

(bought 735350 5/7/2011)

10-5580 MONCTON ST 706000 697000 683000

(bought 740950 2/24/2011)

11-5580 MONCTON ST 711000 703000 688000

(bought 668000 5/3/2011)

8-5580 MONCTON ST 711000 703000 688000

(bought 735350 5/7/2011)

10-5580 MONCTON ST 706000 697000 683000

(bought 740950 2/24/2011)

11-5580 MONCTON ST 711000 703000 688000

(bought 668000 5/3/2011)

E. SFH in Marpole (2012, 2014)

7907 SELKIRK ST 1450000 1387000 (bought: 1570000 5/29/2011)

8043 Montcalm St 1164500 1110600(bought: 1150000 1/18/2011)

8131 CARTIER ST 1333000 1280000 (bought: 1408000 4/19/2011)

8008 CARTIER ST 1548000 1524000 (bought: 1573000 4/19/2011)

7907 SELKIRK ST 1450000 1387000 (bought: 1570000 5/29/2011)

8043 Montcalm St 1164500 1110600(bought: 1150000 1/18/2011)

8131 CARTIER ST 1333000 1280000 (bought: 1408000 4/19/2011)

8008 CARTIER ST 1548000 1524000 (bought: 1573000 4/19/2011)

Thursday, 12 December 2013

BoC confirms "Rate-Hold" phenomenon today

Poloz Says Canada Weighs Risks of Housing Drop

www.bankofcanada.ca/wp...121213.pdf

Dec 12, 2013

As I had predicted this phenomenon back in early July (when rates were just starting to creep up), I'm not surprised. Where I estimated inaccurately was the length of pre-approval (apparently usually 90-120 days), and the ferocity of people applying and exercising their rate-holds.

Here are what the other banks think about this Rate-hold phenomenon:

www.bankofcanada.ca/wp...121213.pdf

Dec 12, 2013

Bank of Canada Governor Stephen Poloz said the central bank’s policy stance is weighing the risk of a sharp correction in the housing market against the threat that price movements will fall into deflationary territory.

Poloz said today home buying has picked up “mainly because people pulled forward their plans when mortgage rates started to move up during the summer. We expect these imbalances to stabilize and then gradually unwind in coming years"

While the central bank’s base case assumes a “soft landing” in the nation’s housing market, “there is a risk that household imbalances could keep building and set the stage for a sharp correction down the road,” he said.

As I had predicted this phenomenon back in early July (when rates were just starting to creep up), I'm not surprised. Where I estimated inaccurately was the length of pre-approval (apparently usually 90-120 days), and the ferocity of people applying and exercising their rate-holds.

Here are what the other banks think about this Rate-hold phenomenon:

Scotiabank: “this would feed into our view that sales rose over the spring and summer at the expense of future months as people exercised options to purchase within 90-120 day mortgage rate commitments on fears of losing the juicy rate commitments back in the spring. I maintain the view that the spring and summer market was a temporary interruption along a correcting sales path”

CIBC: “there’s a huge amount of mortgage debt already in the pipeline that was created when people took advantage of rates they were pre-approved for in the summer. “I’ve seen what is in the pipeline in mortgage activity and you won’t believe the numbers when it is official.”

TD: ““The resurgence in sales activity over the course of this year was likely driven by a frontloading of demand by borrowers with mortgage preapprovals jumping into the market to get ahead of the deterioration in affordability,” Fong said.”

Wednesday, 11 December 2013

Good reads: 1. World's over-valued housing 2. Canadian labor hit by wave of layoffs 3. Canada Post cuts jobs

“Based on their analysis, anyone in the market for property might want to avoid Toronto or Vancouver. On the other hand, if you can get around Japan’s restrictions on foreign investment, an apartment in Tokyo looks like a steal.”

“Although the Deutsche team doesn’t delve into them, it’s not hard to think of some key reasons for these differences. Canada, for example, is very open to foreign investors, which means that in an age of unprecedented global liquidity cash-rich wealthy individuals who are looking for places to park their excess funds can do so in its housing market far more easily than in Japan, with its closed system. ”

“These data also underscore the dilemmas central banks face in various countries. Canada’s, for example, is grappling with a slowdown in its economy and a worrying stagnation in consumer prices that’s raising the risk of deflation. But sky-high house valuations make it difficult for the Bank of Canada to cut rates to spur aggregate demand. A similar problem exists in Australia”

2. Globe & Mail: Canadian labour hit by wave of layoffs, plant closings

Dec. 10 2013

3. Canada Post phasing out home mail delivery, raising rates, cuts 6000-8000 jobs in next 5 years

Work force reductions (since Oct. 1)

3. Canada Post phasing out home mail delivery, raising rates, cuts 6000-8000 jobs in next 5 years

Subscribe to:

Comments (Atom)